10+ Outrageous Deferred Tax Calculation Example Excel Uk

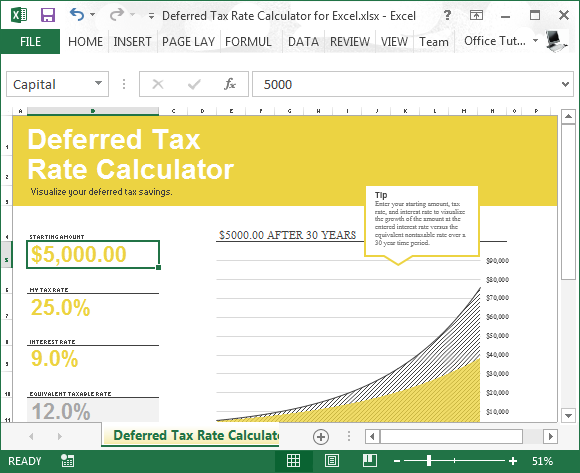

Deferred Tax Rate Calculator For Excel

Deferred Tax Calculation Excel Rocktheme

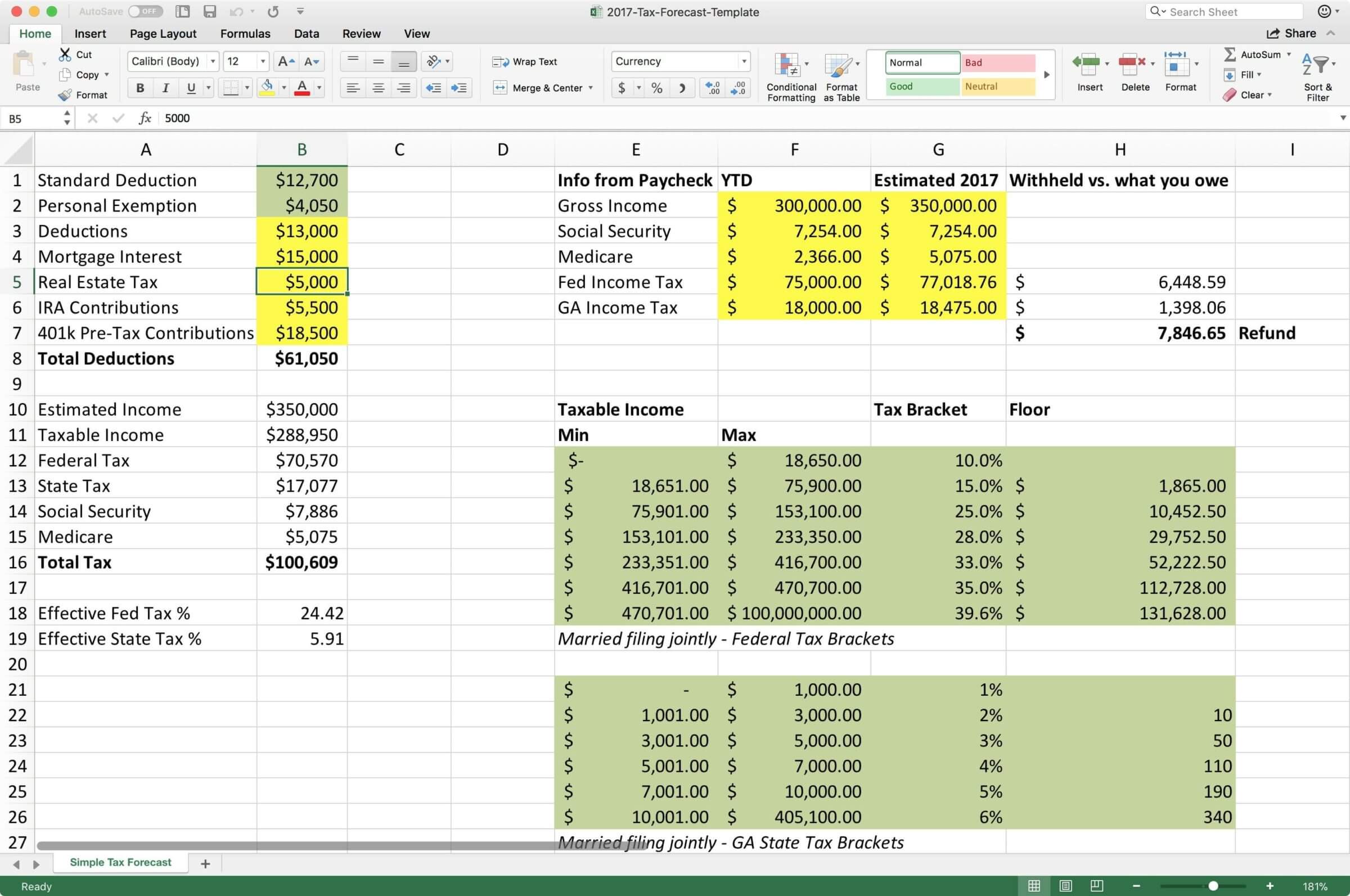

Free Tax Estimate Excel Spreadsheet For 2019 2020 2021 Download

Deferred Tax Calculation Excel Rocktheme

Deferred Tax Double Entry Bookkeeping

Deferred Tax Rate Calculator For Excel

In accounting deferred tax meaning that a liability account on balance sheet that resulted because of the temporary differences between one of the account in accounting could be asset income or etc with the tax carrying the values.

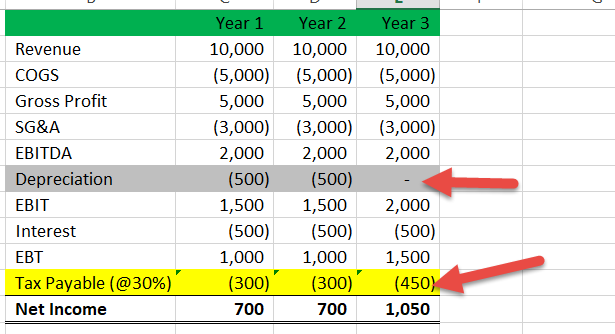

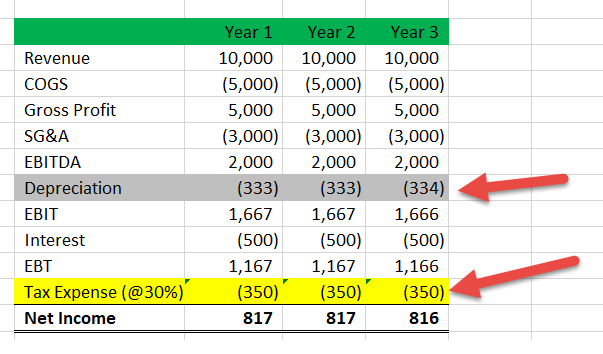

Deferred tax calculation example excel uk. As at 31 December 20X7 it has also claimed tax allowances in excess of depreciation of 60000. Here an effort is made to comprise all tax computation viz Provision for Tax MAT Deferred Tax and allowance and disallowance of Depreciation under Companies Act and Income tax Act in one single excel. I assume they can claim FYA on the equipment.

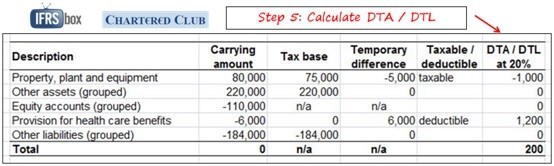

Dep as per Income Tax Act XX Difference in depreciation XX AddLess Other Timing Differences Total Timing Differences Tax benefit loss XX Tax Rate DTLDTA XX. I am preparing a first years set of accounts. Exemption for initial recognition of leases under IFRS 16.

IAS 19 excel examples. This will be recorded by crediting increasing a deferred tax liability in the Statement of Financial Position and debiting increasing the tax expense in the Statement of Profit or Loss. Company A pays tax at 20.

So at the year end the balance is 1700. This excel templates file size is 62896484375 kb. Fair value due to market rate change.

Deferred Tax Calculator is an excel template to calculating the deffered tax of the accounting accounts whether it is assets or income account. Deferred Tax Calculation Example Excel Uk Break clauses where deferred tax purpose of consideration. Would my deferred calculation be as follows.

An excel sheet to better understand the deferred tax calc. Diminishing balance depreciation without residual value. FRS12IAS12 requires several steps in determining deferred tax information first is the construction of a tax balance sheet that involved the determination of tax base for each asset and liability recognised in the accounting balance sheet in order.

Tax Loss Carryforward How An Nol Carryforward Can Lower Taxes

Deferred Tax Asset Journal Entry How To Recognize

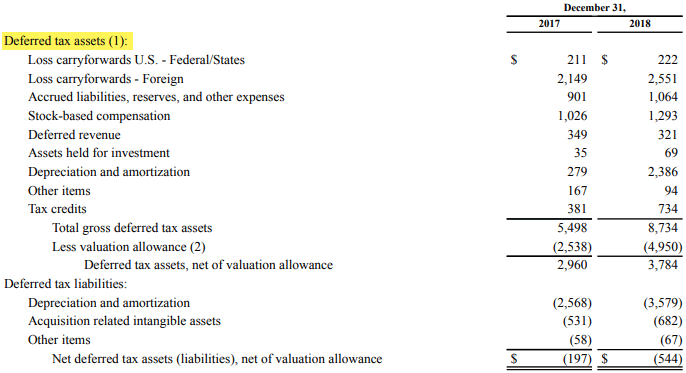

Deferred Tax Liabilities Meaning Example How To Calculate

Deferred Tax Liabilities Meaning Example How To Calculate

Ewell Referent Frugal Deferred Tax Calculation Mentallytoughskaters Com

Deferred Tax Asset Journal Entry How To Recognize

Ewell Referent Frugal Deferred Tax Calculation Mentallytoughskaters Com

Deferred Tax Liability Accounting Double Entry Bookkeeping